The U.S. Dollar is looking in familiar ranges with some movement for petro-currencies as oil and other commodities look to be in the green to start the week.

Overview

Good news out of China improved the mood for Asian equities as well as a contagion of optimism across the European stock exchanges. The world’s second-largest economy is finally taking back restrictions in cities all over the country as the COVID-ravaged economy tries to mount a recovery. Although some economists are pointing at the potential for recession in 2023, few seem to be wanting to be looking that far ahead at the moment.

Without data of any impact until Friday’s inflationary numbers, market sentiment will be mostly guided by news over economic improvements in various regions, particularly China as growth, or lack of it, has been addressed by the government and lending authorities. Meanwhile, in the U.S., recent data suggests that the Fed’s tightening has indeed already started a cooldown for sectors such as housing and even the historically strong labor market. Expect idiosyncratic situations such as political pressures in London to cause more volatility for the Sterling/Dollar pair.

What to Watch Today…

- No major economic events scheduled for today

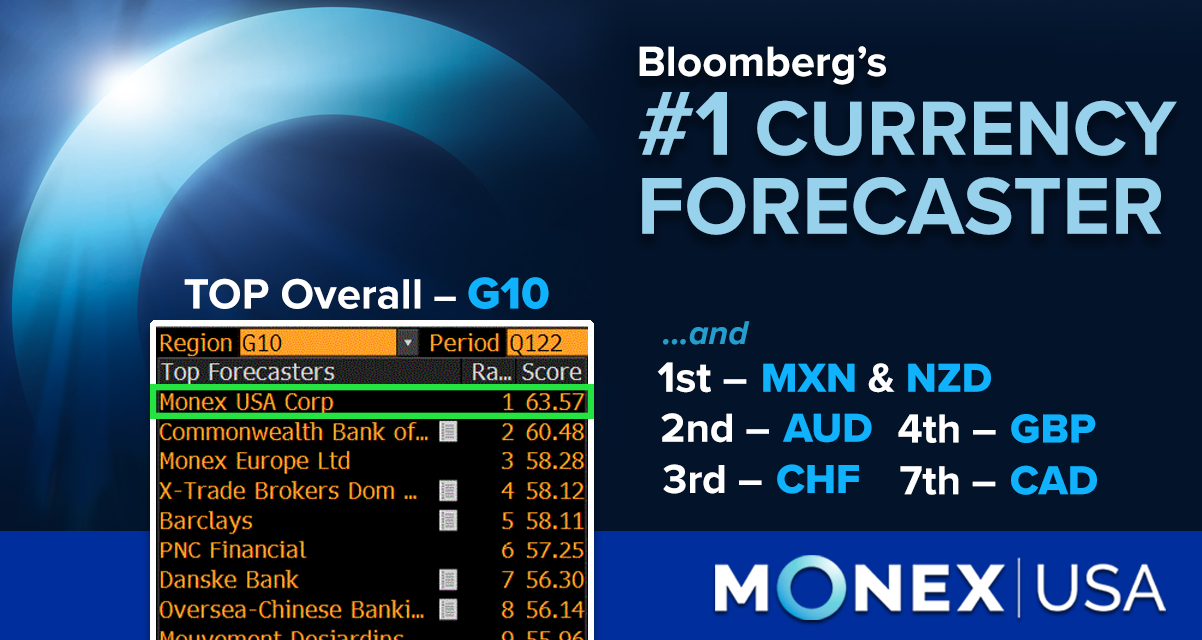

Back to Back TOP Wins | #1 G10 Forecaster for Q1 2022

Bloomberg ranks Monex USA (formerly Tempus) as the top G10 Forecaster, NZD, CHF, AUD, MXN, and GBP! Learn More

EUR

Sterling gained half a percent over the buck this morning as news in the U.K. are all about the potential for a change in government if Prime Minister Boris Johnson were to lose his job. Later today, around 1 PM EST, we should have some word of the results of a Conservative Tory Party Leadership Confidence Vote over the current head of government. Volatility is high in a week that also includes May figures for Purchasing Managers Indices.

GBP

Sterling could easily resume its advancement against the dollar if markets welcome the very positive data presented this morning. A measure of monthly Gross Domestic Product improved by 0.9%, more than double the expected 0.4% for November. It also exceeded the 3-month GDP gauge 1.1% vs. 0.8%. Industrial Production for the month also sky-rocketed with 1.1% over 0.2%. Construction Output was also impressed with 3.5% gain over the 0.6% expected. We shall see if this pushes GBP into higher levels than its best since the end of October.