The U.S. Dollar is trading in tight ranges against most of its peers with the Japanese Yen being the exception following a solid day for domestic equities on the NIKKEI Exchange.

Overview

At the moment, the buck managed to prevent further losses as bets have increased on the Federal Reserve’s future pace of interest-rate hikes. Equities, in general, have failed to flourish as investors weigh the potential effects of tightened monetary policy down the line especially as global food prices, even fertilizer, continue to add pressure on consumers. While equities concern companies, other economists keep pointing at a deceleration of supply-chain concerns, regardless of the fact that China continues to worry about COVID along with other nations.

It is thus unclear to have a long-term picture, but the volatility seen has just become common in this environment. The war has caused a redirection of trade for countries as they seek new energy and food sources after Ukraine and Russia became a conflicted territory. As the world keeps adjusting, expect growth to be the most important metric as we close Q2. We will get data highlighting productivity in the form of S&P Manufacturing Purchasing Managers Index figures for May at 9:45 am, then at 10 AM we will see April numbers for Construction Spending and readings from Institute of Supply Management surveys including prices paid and orders by producers.

What to Watch Today…

- No major economic events scheduled for today

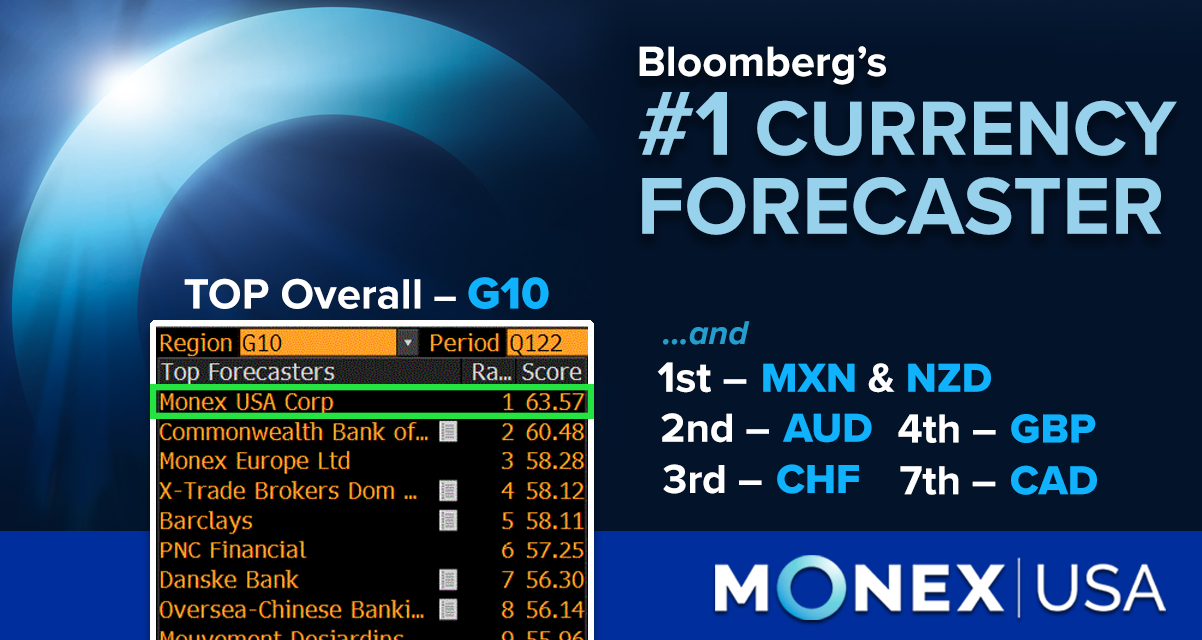

Back to Back TOP Wins | #1 G10 Forecaster for Q1 2022

Bloomberg ranks Monex USA (formerly Tempus) as the top G10 Forecaster, NZD, CHF, AUD, MXN, and GBP! Learn More

EUR

The Euro has not deviated much this morning and could gain more ground-based on increasing bets that the European Central Bank will tighten in July. It is worth noting that the ECB will indeed meet on June 9th, when it is expected that President Christine Lagarde will defend her new directive to get away from negative interest rate territory.

Today’s data showed that the Euro-zone’s Unemployment rate remained at 6.8% after April and S&P Manufacturing PMIs improved slightly from 54.4 to 54.6 from April to May.

CAD

The Canadian Dollar is rising ahead of the Bank of Canada’s policy decision at 10 AM. It is expected that the BOC will sound confident in the current situation and explain that prices need to be combatted with increments in rates. Anything beyond a 50-basis-points hike could send “Loonie” skyrocketing. At the moment of writing, CAD reached its strongest point since mid-April.