The U.S. Dollar is in recovery mode this morning as yesterday’s European and Asian equity sessions failed to continue their momentum into Tuesday.

Overview

U.S. Treasury yields are up while equities are retreating as markets continue to get news over downgraded forecasts for global and regional growth. Officially, the European Union announced a partial ban on Russian oil imports and was able to pass it by giving guarantees to Hungary of leniency. As a result, the price of oil grew to over $120.00/barrel. Additionally, there is evidence of continuing high inflation that has not found reprieve, especially when it comes to food products.At the moment, it looks like stock exchanges may end May with somewhat of a gain after tumultuous times characterized the month. Analysts feel it is indeed difficult to have much clarity about the future as many issues currently seem stubbornly challenging and ongoing. Officials for the Fed have given no indication of getting away from their current hiking path, pointing at the necessary cooling in the Housing sector.

Nevertheless, there is always doubt deep enough economic pressures will force a rethink and if recession looks inevitable, the Fed could change its mind. President Joe Biden will meet Fed Chairman Jerome Powell in an unusual Oval Office meeting to discuss the current inflationary path that is hurting consumers.

What to Watch Today…

- Conf Board Consumer Confidence 10 AM

- Biden-Powell Oval Office Meeting 1 PM

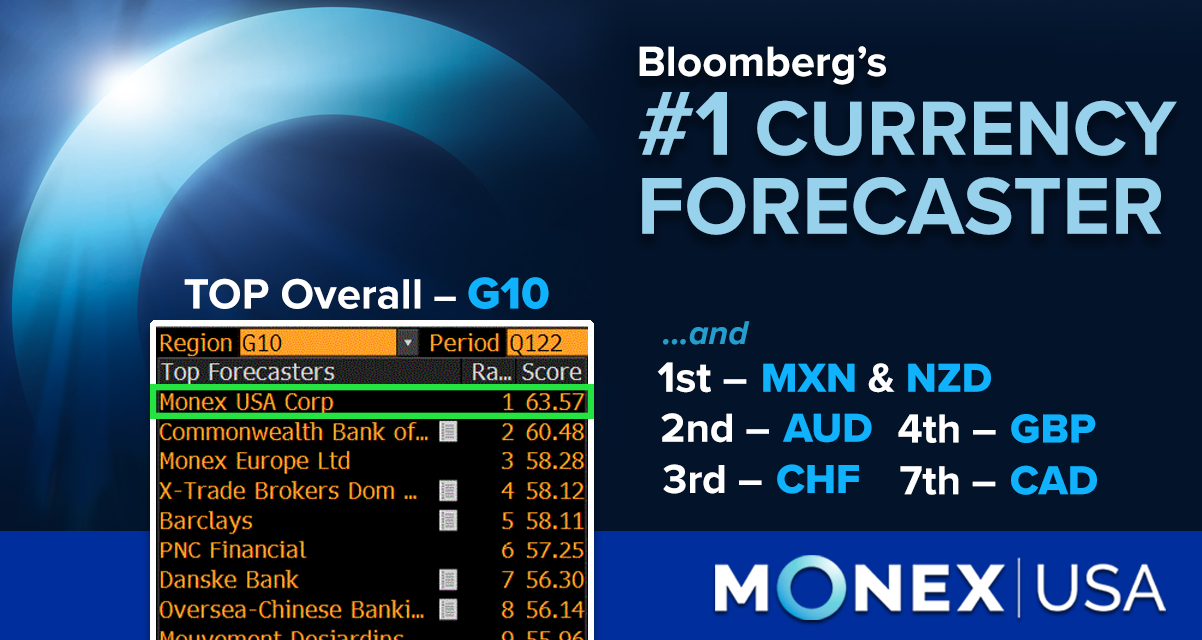

Back to Back TOP Wins | #1 G10 Forecaster for Q1 2022

Bloomberg ranks Monex USA (formerly Tempus) as the top G10 Forecaster, NZD, CHF, AUD, MXN, and GBP! Learn More

EUR

The Euro is dropping today after having gained about half a percent of value on Monday based on the need for the European Central Bank to tighten monetary policy. One thing that helped the Euro recover from its 5-year nadir by mid-month and keep it afloat is the concept of the ECB introducing hikes that will get interest rates above zero, at least away from being in the negative. It is important to recall that the 2008 crisis led to an eventual deluge of monetary aid also in the form of negative deposit rates and the like to encourage financial activity and liquidity.Equities on the other side of the Atlantic have also experienced a bit of a revival, but today the Stoxx 600 halted a four-day streak of gains and declined after reaching its highest point in a month. Euro-zone Consumer Price Index figures grew more than expected at 8.1% over the 7.8% estimate, giving the ECB the green light to guarantee an interest rate increment in July.

GBP

The Sterling has reached its best value in a month but fell as a result of downgraded outlooks and concern that Brexit-related trade issues will hurt the economy. The Bank of England has already predicted a recessionary slowdown into 2023 and the realities of a less-than-desirable trading arrangement are starting to show their toll.

The EU could very well go into high tariff modus operandi if the U.K. refuses to abide by very strict rules that gave the U.K. the benefit of not going into expensive ways to get products from a formerly smooth system with its largest trading partner. Although we are not rooting for the Pound weakening, it may have room to lose as the situation finds little in to be optimistic.